Alan Greenspan’s book The Age of Turbulence raised many interesting issues, one of them was about the behavior patterns on how people adapt to new technology. The formal Fed Chairman asked: Remember the time when answering the telephone was the most urgent thing for you when telephone was just invented? Then when the initial “honeymoon” ended, people began to screen calls and ask to be put on on no-call list.I do not remember that time, but I do recall I used to answer strangers’ emails when email was new. I recall also conversing with a Turkish guy on skype when that was new. Now, like anybody else, I am agitated when spam was not blocked, and only close friends are on my skype contact list. The author concluded: the initial “special treatment” a new technology gets from people is always short-lived. People quickly turn to a more rational way to make a technology serve our human needs.We are seeing today how media is adjusting to new technologies. With many media outlets begin running videos and podcasts on their websites, print journalists are becoming anchors and broadcasters, sometimes to comical effects. If you have seen someone appearing on television for the first time, you know what I mean. Convergence of the media will take place on its platforms and also its practitioners. Wall Street Journal will run print (soon a misnomer), audio and video, the same as CNBC will have all forms of information transmission. And they will hire appropriate professionals for each category.For now, it remains a golden age for print journalists who may want to upgrade to TV reporters (soon a misnomer too).

Live With Technology

Posted in Columns

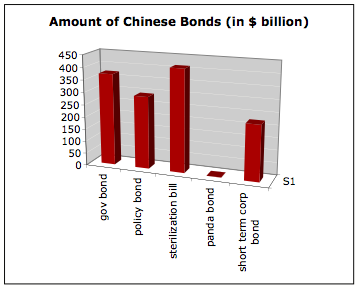

Panda Bonds, Anyone?

China is considering allowing qualified foreign governments to issue yuan-denominated bonds, Finance Minister Xie Xuren said on Saturday. The intention follows the announcement in March that China would allow foreign companies to issue yuan-denominated bonds. So far, these plans are still waiting to be materialized.

The International Finance Corporation, the private sector arm of the World Bank, and Asian Development Bank issued a combined $287.8 million yuan-denominated bonds in 2005. This was the first yuan-denominated bonds issued by non-Chinese institutions, also called Panda bonds, and it remains the only such issuance.More Panda bonds by different foreign entities would bring more variety to China’s bond market and provide investors additional alternatives. The participation of foreign bond issuers could help establish confidence and trust in China’s capital market by the introduction and adoption of international standard of pricing, underwriting, disclosure and documentation.

Panda bond has its limitations, however. The underwriters have been domestic firms and the bonds were traded only on the domestic interbank market. Foreign institutions must invest the proceeds of the bond sales inside China, and cannot transfer them outside. Moreover, the size of the Panda bond can almost be ignored when comparing with other types of bonds.

These limitations are that of the general market condition, of course. As China plans to gradually reform yuan exchange rate, open market access and allow foreign participation, the transition of China’s financial market might be in sight, if everything goes as planned.

Posted in Columns

Futures Market Looking Good?

The Chinese stock market experienced a 4.4% correction last week, the biggest this year. The Shanghai Composite Index dropped 230.07 points to 4984.16 on Thursday amid light trading. While the stock market may look bearish, China’s futures market is gaining momentum.

Trading value on the Shanghai Stock Exchange moved around $50 billion Yuan per day at the end of last week. The futures market trading value stood at 328 billion Yuan per day, six times more. During the past twelve months, the futures market trading value increased 139%, while the stock market trading dropped since peaking in June.

Chinese Futures and Stock Market Trading Value (Billion Yuan)

(Source: China Securities Regulatory Commission. Copy right reserved by Red Capitalists)

This may reflect a shift in strategy among investors. Many consider the stock market overvalued and expect further corrections. With few alternatives, the futures market appeals to investors because China’s strong demand for metals, rubber and soybeans is expected to continue.

The futures market is off limits to foreign investors and participants. Only foreign companies who have a legal status in China could trade in the futures market. This makes it more isolated. Foreign investors could invest in China’s stock market through certain programs.

There are three commodity exchanges in China in Shanghai, Dalian and Zhenzhou. They trade in aluminum, rubber, fuel oil and soybeans, among others.

Golden Oil and Iron Triangle

Oil at $100 a barrel and gold at $850 an ounce? Dollar at 1.5 against Euros? These were the speculations ran wild during the past week. Before trying to address these questions, what are the relationships between oil and gold, dollar and Euro, interest rate and inflation?

Historically, the Queen of metals (gold) and the King of commodities (oil) tend to dance together, with the oil/gold price ratio at an average of 15:1. The price of oil has significant implication for inflation. An increase in oil not only translates into more expensive transportation, utility and heating for consumers, it also pushes up cost (both for the production and distribution) of virtually every consuming products. When oil price goes up, the pressure of inflation is on.

Contrarily, gold has complex implication for currency. Before 1971, U.S. dollar was backed by gold and the price of gold was fixed at $35. That year, the U.S. abandoned gold convertibility. Four years later, OPEC officially agreed to accept U.S. dollars as the exclusive payment for its oil, scrapping gold as the mean of exchange. These changes caused a shake up in oil and gold’s prices in dollar. Oil soared to $40 from $3 per barrel; gold flew from $35 to $850 per ounce.

Generally, when oil price goes up, people start worrying about inflation. While fear of inflation pushes people to invest in gold to offset the effect of inflation, hence driving up the price of gold.

Now, how did the U.S. dollar become so weak? There is a law in economics called the Iron Triangle. It says among a currency’s interest rate, exchange rate and convertibility, only two can be achieved. It is impossible to achieve (or control) all three elements. The U.S. dollar is fully convertible and the Federal Reserves sets the interest rate. It means that when the Fed cut interest from 5.25% to 4.5%, the dollar has to become weaker.

A lower interest rate stimulates the economy, but it is also innately inflationary because in order to lower the interest rate, more money has to be bumped into the economy. A weak dollar could help to correct the U.S.’ trade deficit, but it also tends to drive up prices simply because of the paper money is worth less – rather than a result of supply and demand.

Put everything together, expensive oil, expensive gold, lower interest rate and a weak dollar are all harbingers of inflation. The Fed’s interest rate cut made the dollar weaker, and it drove up the prices of oil and gold, which translates into possible inflation. Some may view this as iron evidence for a new world of high inflation from now on. It may be true if you still believe the world of dollar hegemony is going to continue. The question becomes is it? With OPEC and other emerging markets prepare to diversify their currency holdings from a single U.S. dollar, the dollar dynasty may well be toward an end.

Posted in Columns

Hot Economy, Hotter Interest Rate?

China said on Thursday that the economy grew 11.5% year-on-year in the third quarter, slightly lower than the second quarter’s 11.9%. Inflation was up 6.2% from a year earlier, down from 6.5% in August. The news unleashed different reactions. Some predicted China’s Central Bank would increase interest rates immediately; others were more optimistic that the economy is finally showing signs of a gradual slow down.

Those who anticipated a rate rise should bear in mind a caveat. China had increased the key one-year bank-lending rate five times to 7.29% this year, each time the stock market soared on the news. In the first ten month this year, fixed asset investment rose 26.9% to $1.2 trillion, among which real estate investment surged 31.4% to $256 million. The rate hikes seemed unable to put a brake on China’s hot economy.

One explanation could be that an interest rate increase in China is more symbolic than functional, at least under the current market condition. The two main drivers of China’s economy have been investment and export. In the first nine months, actual foreign direct investment grew at 11% to $6 billion, less than half of fixed asset investment growth. China’s investment boom is more and more driving by domestic investment in property and infrastructure, and the real estate developers and local governments are unlikely to have a 27 basis point interest rise stop their party. On the other hand, factories continue to churn out goods. China’s export rose 26.5% in the first ten months.

A higher interest rate has only nominal effect on China’s money supply. An interest rate adjustment, when working in a market economy, alters money supply and therefore affects consumption and investment. But China’s Central Bank had issued massive amount of sterilization bills to prevent Yuan’s appreciation. In 2006, such bills amounted to $414 billion, almost a quarter of the year’s M1 supply. The effect of an interest rates adjustment on money supply could almost be ignored.

Increasing interest rates also does little to affect consumer prices as China imposes direct price control on core consuming goods, such as gasoline, medicines, rice and cotton. When oil surged toward $95 per barrel last week, the price in China was fixed around $60. The government last month released reserve pigs to retain pork prices. When prices are unable to reflect market conditions, the effect of interest rates adjustments will be compromised.

No evidence suggests that higher interest rates are discouraging bank lending. Chinese banks made $471 billion new loans in the first 10 months, a 15.6% increase from a year earlier. Similarly, households are unlikely to save more because of higher interest rates. With China’s stock market red hot, millions of Chinese are betting on the stock market.

While people await the Federal Reserve’s decision at the end of the month, it is important to recognize that a rate hike in China may mean different things. Rising interest rates is a good gesture of the Chinese government. But as long as China’s economy maintains these characters, raising interest rates is the wrong cure for the problem.

Posted in Columns

Recession Talk Is Just Talk

October 19 2007 – the twentieth anniversary of Black Monday – saw the Dow Jones Industrial Average shed 367 points, or 2.64%. That is modest comparing with 1987’s historical market crash, in which the Dow free-fell 22.6% to evaporate around $500 billion market value. But today’s situation may be worse in its enormous uncertainty. Instead of an epic crash right in the beginning and in one crisp drop, the market today is fraught with fear: is the worst still ahead? If it is, when?

Since the beginning of the year, sentiment has been swinging. The past week may be the nadir so far. The pessimists made the loudest noise, deafening the optimists and the middle ground camp. CEOs, economists and poll result that believe a recession is near made the headlines, well fitting to the stock market down turn. Of course, when the market goes up, bet the optimists to gain the dominant voice.

Who is right in the mist of the guessing game? The Caterpillar CEO Jim Owens who believes the U.S. is near or already in a recession, or the International Monetary Fund who lowered the economic outlook but maintained a moderate growth next year? Moreover, is economic reality perceivable?

Listen to Fed chairman Ben Bernanke. In an academic and invitation only conference in St. Louis, Bernanke combed through past research and studies on monetary policy last Friday. The chairman avoided speaking for himself in a strict “literature review” style and terminology-filled talk. But he did make certain about one thing: uncertainty.

“Uncertainty about the current state of the economy is a chronic problem for policy makers,” Bernanke said. “At best, official data represent incompetent snapshots of various aspects of the economy, and even then they may be released with a substantial lag and be revised later.”

This resonates with what happened last month when the Labor Department revised payroll figures in August from a net loss of 4,000 jobs to 89,000 gains. The chairman then looked back on efforts to respond in the face of two other economic uncertainties: the structure of the economy and the way in which the public form expectations about future economic developments and policy actions.

But the bottom line, Bernanke stressed, is that “uncertainty…is a pervasive feature of monetary policy making.” The uncertainty includes the state of the economy, the economy’s structure and how the public would react. Fundamentally, the chairman ended: “our discussion of the pervasive uncertainty that we face as policymakers is a powerful reminder of the need for humility about our ability to forecast and mange the future course of the economy.”

Compare this with Caterpillar’s Jim Owens’ scary prediction. At least Bernanke is honest that he does not know the future.

Posted in Columns

Faster Yuan Appreciation Ahead?

Europe is getting jittery about China’s yuan. This year, the continent imported more Chinese goods than any other country except the United States. European Union’s trade deficit with China is also growing at two times faster than that of US.

This new evidence has reaffirmed politicians and economists’ belief that the Chinese yuan is greatly under-valuated. No one disputes that. But problems arise when the question comes to how fast the yuan should appreciate.

The U.S. has been pressing China to appreciate its currency for years. Only recently has the focus of negotiation moved to the pace of change. Now Europe is joining in. But Chinese policy-makers are uncompromising of a moderate approach, citing Japan as a deterrent example.

The currency relationships among the world’s largest trade bodies indicate worse is still ahead, if action is not taken soon. Europe is in the least favorable condition. The Euro gained 14% against the dollar and 5% against the yuan in the past two years, making European products more expensive. As a result, Europe’s trade deficit with China is widening fast, while its trade surplus with the U.S. is closing. The U.S. has a trade deficit with both China and the EU. (See charts )

As a result, the world is seeing the worst account imbalance in history. As American consumers and government keep borrowing, the Chinese government piles up dollars in its foreign reserve – not only cumbersome to manage but creates zero value (when considering inflation, its value decreases). At the same time, with the yuan under-valued, Chinese consumers still refrain from consumption, and maintain high savings rate.

So, are there middle grounds for the negotiators? Plenty. The yuan gained over 9% in the past two years, while at one point, the Japanese yen was gaining 15% over three months in 1999. Now with EU’s account balance on the line, a stronger Yuan may be just ahead.

Posted in Columns

How Long Will The Party Last?

The Chinese stock market is unquestionably the hottest market this year. While most other markets suffered from the credit squeeze originating from the U.S. subprime mortgage mess, the Shanghai CSI 300 index shoot up roughly 2500 points, doubling the indicator.

Many economists and analysts, based on the hefty evaluations of the Shanghai market, believe a correction is ahead – and soon. Stocks on the CSI 300 index sell for an average 44 times of earnings, compared with 26 times for H shares in Hong Kong, according to Bloomberg.

While no one can predict the market, a little history helps the analysis. The longest and strongest bull run in New York Stock Exchange was the 1990s. During that ten years, the Dow Jones Industrial Average Index rose from roughly 2700 to 11700, a 333% increase. For Tokyo Stock Exchange, the Nikki index increased from roughly 6600 to 23700, an increase of 259% from 1980 to 1990 – the most spectacular growth in the market’s 129-year history.

The CSI 300 Index in Shanghai, in comparison, witnessed a growth of 485% in less than two years. It jumped from 940 in 2006 to 5,500. It is the most dramatic bull run the world has ever seen. If the Shanghai market keeps the current growth speed, the market index would jump 685100% to

6,441,546 in 10 years. Clearly, it is impossible.

So, does that mean an dreadful market crash is looming soon? If history is any guide, the New York and Tokyo bull run both ended with spectacular crashes.

Posted in Columns

China’s Mega Financials

The importance of China’s financial market is open to question, but its gigantic size is hard to neglect. Industrial and Commercial Bank of China (ICBC) issued the biggest initial public offering the world has ever seen by raising $19 billion last year. China Shenhua Energy Co. raised $8.9 billion last week in the biggest IPO this year worldwide.

Big deals have created big brokerage firms. Citic Securities, a 12-year-old Beijing brokerage firm, is now the fourth largest brokerage firms in the world, trailing only behind Goldman Sachs, Morgan Stanley and Merrill Lynch – star brokerage firms of Wall Street with an average history of a hundred years. Shanghai-based Haitong Securities ranks the eighth biggest worldwide.

A trend easy to discern is that Chinese mega deal-makers favor Chinese underwriters. China International Capital Corp (CICC) and China Galaxy Securities underwrote Shenhua Energy IPO. Three Chinese brokerage firms underwrote the second largest IPO in China – that of China Construction Bank. In the top ten equity offering deals this year, the majority underwriters are Chinese firms. Goldman Sachs, Lehman Brothers, HSBC and Citi each appeared on the list once, in a consortium.

In other types of financial intermediaries, China is more visible as well. China’s four national banks are among the world’s biggest banks. At current market price, ICBC is the world’s biggest bank by market capitalization, bigger than Citigroup.

China also boosts Asia’s biggest sovereign wealth fund – China Investment Corp. The fund started operation last Friday with $200 billion capital under management.

China Life – the country’s largest insurance company – is expected to outsize AIG, the world’s biggest insurance company. AIG’s market capitalization is $173 billion, while China Life is $162 billion.

The emergence of large Chinese financials is probably the single most important event during the past several years. It is changing the landscape of world finance. Moreover, these monstrous firms are growing at an extraordinary speed.

But veteran capitalists need not to worry yet. Although they are big and are getting bigger, it is uncertain that these Chinese firms’ impact will be felt outside of China any time soon.

Posted in Columns

The Buffett Dilemma

Warren Buffett, the legendary investor and second richest man in the U.S., trimmed his company’s holding in PetroChina three times in the past two months. The sales of 138 million PetroChina shares brought a profit of $183 million, a 925% return.

Berkshire Hathaway, where Buffett is CEO, remains the second largest shareholder of PetroChina, after China National Petroleum Corporation (CNPC), a 100% Chinese government owned enterprise.

The billionaire bought the shares at 1.6 Hong Kong dollars per share in April 2003. The shares were sold in July, August and September for prices ranging from 11.47 to 12.4 Hong Kong dollars. Berkshire’s share in PetroChina dropped from 11.05% to 8.93% after the sales.

The simple profit taking, unexpectedly, has been lauded by human rights groups who cheer for Berkshire’s divesting from a Chinese company that has afflicted operations in Sudan, where millions of people were displaced and grave killings took place during the Darfur crisis.

There was enormous opposition since the company’s investment in PetroChina. In May, 809,995 A-share Berkshire holders and 8,471,129 B-share holders voted on a proposal to divest from PetroChina. Buffett, in a shareholder letter, listed three reasons to vote against the proposal.

First, it is PetroChina’s parent company, CNPC, who does business in Sudan – not PetroChina. In the same way that the U.S. government created Fannie Mae and Freddi Mac, CNPC may shape or control PetroChina’s operations, but PetroChina should in no way be responsible for what CNPC does.

Second, an investor should not divest because he or she disagrees with an investee’s certain activity. The letter pointed out that the shareholder who proposed to divest from PetroChina did not divest from Berkshire because she disagrees with its investment decisions.

Finally, even if CNPC stops its operation in China, there is no guarantee that the situation in Sudan will improve. That is because CNPC owns 40% of a Sudan venture whose primary assets are oil and fixed assets (oil refinery and transportation equipment). Therefore, the feasible divestment plan for CNPC would be to sell its 40% invest to the Sudanese government. The consequence would only make the Sudanese government financially stronger – but does that help the conflict?

The result: 97.5% shareholders voted against the proposal, and 1.8% voted for it.

The vote settled the issue – or Buffett may wish. Human rights groups continue calling Berkshire to divest from PetroChina. But many agree: the recent selling is just profit taking. Or who knows – maybe Buffett changed his mind on Darfur?

Posted in Columns